For years, tolling agencies have evaluated payment technology primarily through the lens of transaction fees. As long as toll revenue is ultimately collected and systems continue to operate, existing payment arrangements are often considered sufficient. This mindset—rooted in a justifiable desire for reliability and risk avoidance—has resulted in highly fragmented payment environments made up of multiple processors, vendors, channels and legacy systems.

While these environments may appear stable, they obscure a broader and more consequential reality: transaction fees represent only a fraction of the true cost of accepting payments. Research into tolling payment behavior shows that friction in the payment experience—not unwillingness to pay—is a major driver of revenue leakage. Nearly 40% of drivers report difficulty navigating toll agency payment websites, and almost half say an easier payment process would have helped them avoid a past-due toll or violation.

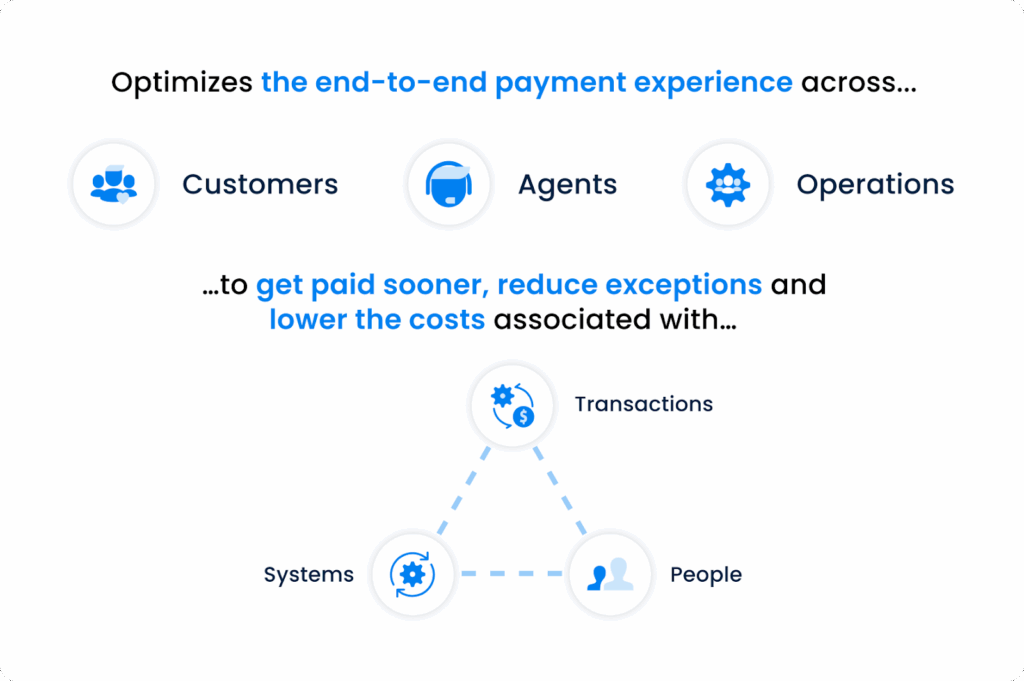

This paper introduces the concept of the total cost of payment acceptance, and examines how three core cost categories—transaction costs, people costs and systems costs—shape the economics of toll collection. It also explores why a more integrated approach, known as Payment Experience Management, can help tolling agencies reduce long-term costs while improving operational performance and driver satisfaction.

Key takeaways

Tolling agencies will learn:

- Why transaction fees alone understate the true cost of payment acceptance

- How transaction costs, people costs and systems costs combine to drive cost of collection

- Why payment friction and exceptions fuel toll revenue leakage

- How failed payments escalate into violations, service calls and collections activity

- Why tolling faces greater exception sensitivity than retail or lending

- How Payment Experience Management reduces total cost by improving success rates, lowering operational workload and simplifying technology environments

The status quo in tolling payments: Stable, familiar—and expensive

Tolling agencies operate in environments that reward stability, auditability and procedural rigor. Procurement cycles and request for proposal (RFP) processes are long, stakeholder groups are large, and changes invite scrutiny. As a result, agencies rarely revisit payment systems unless a visible failure forces action.

Over time, most agencies have assembled payment stacks incrementally: one processor for cards, another solution for ACH, a separate Interactive Voice Response (IVR) platform, a retail cash partner and disconnected online portals. Each component functions independently but few operate as a coordinated whole.

Agencies accept the operational burden of reconciling data, managing vendors and resolving inconsistencies because the systems technically work. Yet fragmentation increases costs, slows innovation and limits visibility into overall payment performance.

Moving beyond transaction fees

In tolling, where margins are closely scrutinized, minimizing per-transaction cost can feel like the smartest, most responsible decision.

But transaction fees alone provide an incomplete—and often misleading—picture. A payment that appears inexpensive on paper can become costly if it fails, is delayed or requires manual follow-up. When viewed across millions of transactions, these inefficiencies materially impact the cost of collection, cash flow timing and staff workload.

To evaluate payment economics accurately, agencies must look beyond per-transaction pricing and examine the total cost of payment acceptance.

Defining the total cost of payment acceptance

The total cost of payment acceptance includes every cost required to collect, settle and reconcile a payment successfully. While transaction fees matter, exception handling often drives the largest expenses.

Three categories shape total cost:

- Transaction costs – direct processing expenses including retries and disputes

- People costs – labor required to manage exceptions, support drivers and reconcile data

- Systems costs – technology, integrations, maintenance and vendor coordination

Payment exceptions, meaning any instance where a payment does not complete as intended, drive costs upward across all three categories.

Transaction costs: More than a per-swipe fee

Transaction costs are the most visible component of payment acceptance. Because they are easy to quantify and benchmark, transaction costs often dominate procurement evaluations. But in reality, there may be hidden costs and benefits with each tender type in the payment mix.

- Traditional ACH is typically a low-cost option, but lower transaction fees come with tradeoffs. ACH is not real-time and can take a few days to settle. And because bank balances fluctuate, ACH can result in a high number of non-sufficient funds (NSFs) or administrative error exceptions.

- Debit and credit cards are widely used by consumers, but can be subject to chargebacks, fraud and low account balance risks for debit.

- Apple Pay and Google Pay securely store customer cards and process at standard card rates. The stored cards often represent a customer’s preferred way to pay, boosting payment completion. While still vulnerable to the drawbacks of debit cards, they offer additional layers of security and documentation that improve their reliability for card-not-present transactions.

- PayPal, Venmo and Cash App Pay may carry higher transaction fees. But for consumers who store balances in these wallets, they can be the lowest-cost way to complete payment. If wallets accelerate payment or prevent exceptions, the effective cost is lower.

In practice, transaction costs rarely end with the first attempt. A Pay-by-Mail customer may submit a card that declines, retry with another card, then abandon the process. An IVR caller may mistype information and attempt payment multiple times. Each attempt incurs cost without generating revenue.

Retries, chargebacks and reversals increase effective processing expense and delay settlement. When agencies lack intelligent routing or flexible payment options, approval rates suffer and retry volume rises.

Over time, low per-transaction pricing can mask high cost per collected dollar.

People costs: the hidden driver of collection expense

People costs represent one of the largest—and least visible—contributors to the total cost of payment acceptance in tolling. These costs include the internal labor required to manage payment exceptions, support drivers, reconcile transactions and coordinate across vendors.

Violation escalation loops further amplify these costs. When a payment fails and is not resolved quickly, it can progress from an initial invoice to a violation notice, then to collections. Each step increases handling effort, call volume and administrative overhead—often far exceeding the value of the original toll.

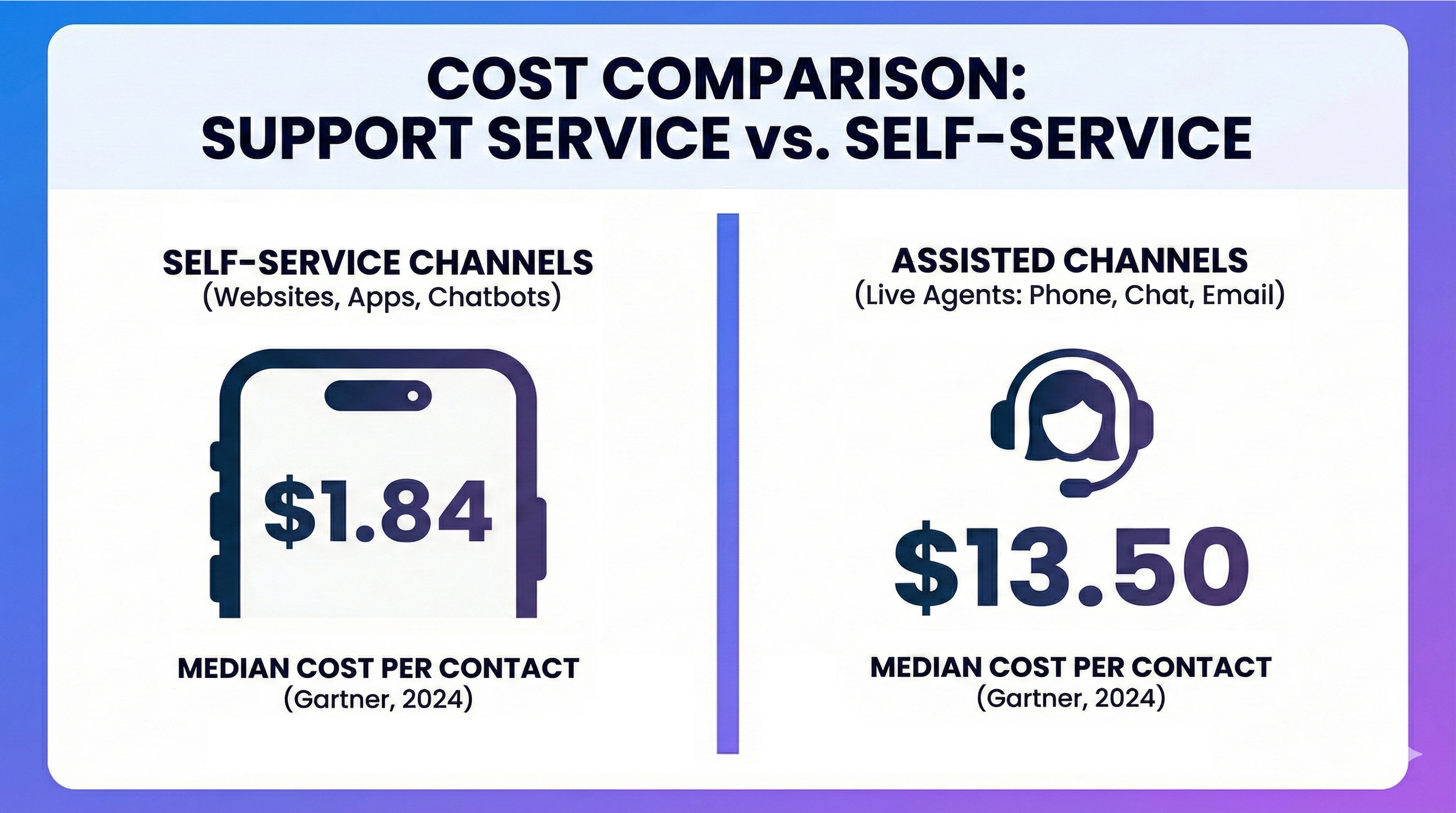

The hard costs of these support interactions are undeniably high. According to Gartner, the cost of an average customer service interaction is approximately $13.50, while a comparable self-service interaction weighs in at about $1.84. This significant increase can be one of the biggest cost drivers for an agency, especially as all-electronic tolling (AET) pushes drivers to adapt to a new way of paying for tolls.

As agencies add payment channels without centralized management, people costs scale disproportionately. The expansion of AET—combined with legacy systems that generate high support volumes—drives call center strain, burnout and turnover.

According to CallCriteria, the financial impact of high turnover extends far beyond recruitment costs. Replacing a single call center agent costs $10,000-$20,000 when accounting for recruiting, hiring, and training expenses. For a 100-agent call center, the full impact including lost productivity and customer satisfaction can reach $1 million or more annually.

A modern, self-service payments platform significantly reduces call volumes, enabling more cost-efficient workflows and less stress on support agents. This allows agencies to operate with fewer entry-level staff while reallocating experienced collectors to focus on personalized customer engagement to improve recovery for unpaid violations.

Systems costs: Paying to maintain fragmentation

Systems costs encompass the technology, integrations and infrastructure required to support payment operations. In tolling, these costs are often distributed across gateways, processors, IVR platforms, cash networks, mail vendors and commercial back-office systems.

Most tolling agencies manage multiple contracts, data feeds and reconciliation processes for all of these disparate systems. Even modest changes—such as adding a wallet or modifying a portal—can require cross-vendor coordination, testing and procurement approvals.

This fragmentation limits agility and increases long-term maintenance expense. Agencies invest time and money maintaining integrations instead of improving performance. As tolling agencies move toward cashless roads and digital-first engagement, these rigid architectures become increasingly difficult—and expensive—to adapt.

The high stakes of exceptions in tolling

Underneath all three of the cost categories discussed—transaction costs, people costs and systems costs—lies the driving force behind increased costs: Exceptions. Payment exceptions, or any time a payment isn’t completed as expected, come with high impact in the tolling industry. Because tolls are usage-based and frequently postpaid, exceptions compound over time. A small-dollar transaction can evolve into a high-cost enforcement process involving multiple notices, retries, disputes and service interactions.

This compounding effect makes tolling uniquely sensitive to payment friction.

To understand why exceptions have such an outsized impact in tolling, it’s helpful to look more closely at the different types of exceptions agencies face and how they drive costs across the payment lifecycle.

Understanding exception costs in tolling

Toll collection would be far simpler if every toll were paid on time, every time. In reality, exceptions are unavoidable—but not all exceptions are created equal. Some arise from genuine account conditions such as insufficient funds, while others result from preventable friction in the payment experience. The former are considered traditional (true) exceptions, while the latter are “experiential.”

Traditional exceptions include returns, disputes and authorization failures. Experiential exceptions occur when drivers encounter confusing portals, restrictive payment flows or unnecessary login requirements that cause them to abandon or delay payment.

Experiential exceptions are often preventable and therefore represent the greatest opportunity for the reduction of payment costs and revenue leakage.

NSF returns and failed payments

Non-sufficient funds (NSF) returns can occur across several tolling payment methods, including ACH, debit and bank transfers. For this reason, tolling agencies often avoid ACH as a primary payment method for auto-replenish customers because of potential operational headaches despite its low processing cost. When an ACH payment fails, agencies incur return fees, retries and potential escalation into violation workflows.

Because ACH operates on delayed settlement timelines, agencies may not learn of failures for days. During that time, unpaid tolls may progress through billing stages, increasing administrative cost. Without automated retry strategies and intelligent monitoring, low-cost payment methods can become high-cost recovery efforts.

Chargebacks and disputes

Drivers initiate chargebacks when they do not recognize a descriptor, question a penalty or misunderstand a billing timeline. Resolving disputes requires documentation, staff time and system coordination.

Clear descriptors, transparent notices and accessible payment histories reduce preventable disputes, while centralized data improves response speed and increases successful outcomes. At the end of the day, preventing disputes costs less than resolving them.

Exceptions driven by poor payment experiences

Experiential exceptions introduce the greatest opportunity for improvement. These occur when drivers are discouraged by payment hurdles that cause them to postpone payment, abandon the process or resort to calling an agent.

Agencies should consider all of the following drivers of experiential exceptions:

- Friction-filled user experience. Consumers expect seamless payment experiences like those in eCommerce. Entering login credentials, invoice numbers or lengthy account details can frustrate customers, especially on mobile devices.

- Limited payment options. Many consumers now prefer to use mobile wallets as their primary bank account. Tolling agencies that only accept cards or bank account create unnecessary friction, and may even increase NSFs and violations.

This issue is particularly significant for low-income or underbanked drivers who need or prefer to pay with mobile wallets or cash. - Lack of information and communication. A number of late payment exceptions are due to the difficulty of keeping track of invoices and due dates. Providing actionable reminders and clear explanations for declines can empower customers to resolve issues on their own, reducing support calls and speeding up payment completion.

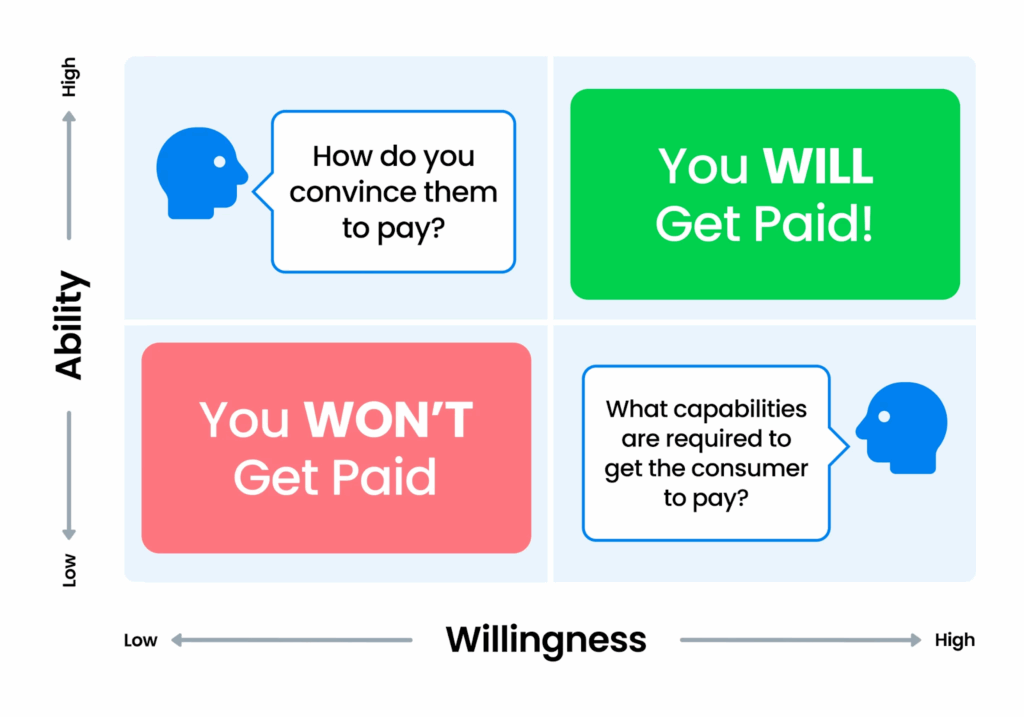

Poor payment experiences can shift drivers within the classic “Willingness & Ability” framework. A driver who is both willing and able to pay may become unwilling when the process feels overly complex. Others may intend to pay later and unintentionally fall into violation status.

In fact, 49% of drivers surveyed in PayNearMe’s tolling research stated that “an easier payment process that isn’t long or complicated” would have helped them avoid receiving a toll violation.

Reducing experiential exceptions requires designing payment experiences that meet drivers where they are—offering flexibility, clarity and simplicity across channels. In tolling, this is one of the most effective levers agencies have to reduce exception volume and control long-term costs.

Payment Experience Management: Reducing costs across the board

Payment Experience Management provides a unified approach to managing the total cost of payment acceptance by directly addressing transaction, people and systems costs.

From a transaction cost perspective, Payment Experience Management improves payment success rates through intelligent routing, broader payment choice and optimized flows across channels. Fewer declines and retries mean lower effective processing costs and faster access to funds.

From a people cost perspective, centralized visibility and automation reduce the need for manual intervention. Exceptions are identified earlier, reconciliation is streamlined and customer service teams see lower call volume and spend less time resolving avoidable issues.

From a systems cost perspective, Payment Experience Management acts as a unifying layer rather than another silo. Agencies gain the flexibility to add or modify payment methods without re-architecting their entire environment. Reporting, compliance and performance management are handled centrally, reducing long-term technology overhead.

By addressing all three cost categories together, Payment Experience Management shifts the economics of toll payments from reactive exception handling to proactive optimization.

Short-term cost vs. long-term economics

Tolling agencies operate within rigorous procurement and governance frameworks. RFP processes, legal review and multi-stakeholder approvals make change deliberate and often slow. When systems function and audits pass, agencies often prefer the status quo.

This caution encourages short-term cost comparisons. Transaction fees are easy to document and defend. Operational savings—reduced call volume, fewer violations, faster settlement—are harder to quantify during procurement and therefore receive less emphasis.

However, fragmented systems distribute costs across departments and budgets, masking their cumulative impact. Manual reconciliation, exception handling and enforcement workflows quietly inflate cost of collection.

When agencies evaluate payments through a total-cost lens, the economics shift. Higher success rates reduce exception volume. Lower call center demand frees staff for higher-value work. Improved settlement predictability strengthens cash flow. Flexible architectures reduce future procurement cycles.

While sophisticated platforms may carry higher visible costs, long-term gains often outweigh incremental fee differences. The real risk may lie in preserving the status quo.

The benefits of a platform built on Payment Experience Management

Offer more options to improve on-time payments

Providing more payment types reduces risk, exceptions and delinquencies by meeting customers where they are.

A modern fintech platform enables you to accept a full range of payment types, including ACH, cards, digital wallets, and even cash at retail locations including Walmart, 7-Eleven, Walgreens and others. The goal is to optimize the payments mix for each customer, maximizing on-time payments and minimizing costs.

Provide personalized links for seamless self-service

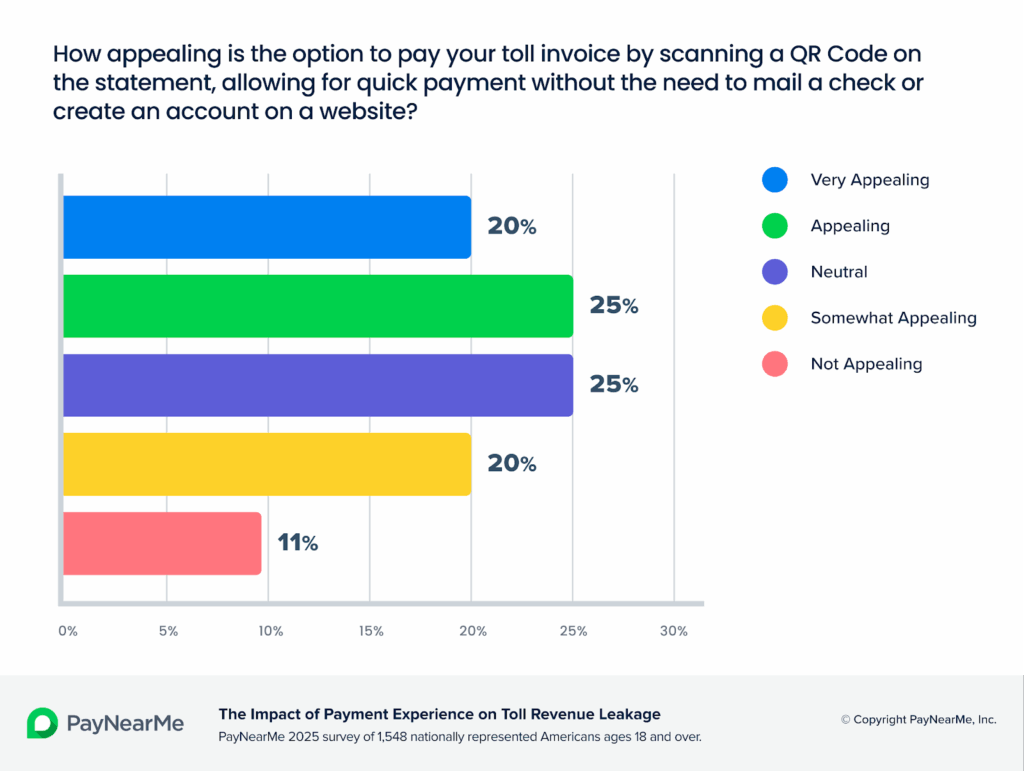

Personalized payment links enable customers to complete payments easily and securely without needing to log in. This addresses a major pain point: 39% of surveyed drivers stated that accessing the toll agency’s website or payment portal makes paying a toll invoice difficult or frustrating.

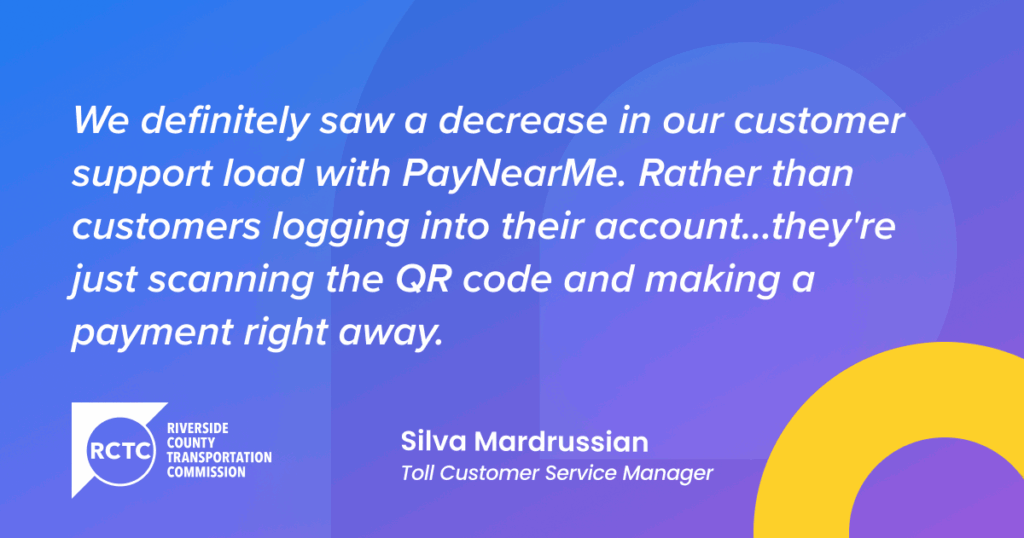

Personalized payment links via QR codes printed on invoices helped one of PayNearMe’s tolling clients, The Toll Roads, collect more unpaid tolls significantly faster. The Transportation Corridor Agencies (TCA) planned, built, financed, constructed and continue to operate the roads, which make up 20% of Orange County’s highway system. For drivers who prefer using cash or having an additional option to pay tolls, replenish a FasTrak account or resolve a toll violation, TCA expanded its appeal to consumers by partnering with PayNearMe.

With the introduction of QR codes, TCA anticipated a 5% bump in payments made through PayNearMe and, instead, is experiencing a 640% increase. The Agencies also saw a 35% increase in payments from drivers who didn’t initiate toll payment within five days of driving The Toll Roads.

Send digital reminders to reduce violations

Half (50%) of surveyed drivers report that receiving a text message (SMS) with a direct payment link would be their preferred method of receiving payment-due notifications or invoice reminders. Automated, personalized reminders can improve on time payments and streamline follow-ups for past-due accounts collection times.

Hyper-personalize to influence payment behavior

Payment data reveals customer preferences and patterns. Agencies can prioritize preferred methods, reduce friction and improve success rates across segments. By combining intelligent tools with driver-centric experiences, agencies reduce total cost of acceptance across all categories.

Automate payment optimization with business rules

Data-driven rules can leverage customer behavior and payment information to help reduce risk. For instance, logic rules can identify customers with multiple NSFs and preemptively offer alternative payment options. Automated rules eliminate manual intervention, greatly reducing staff time and effort.

Reduce downtime with smarter routing

Redundant processing paths and intelligent routing maintain continuity during outages, when agencies normally face lost revenue, post-outage support call spikes and missed payment opportunities.

A platform with baked-in redundancy and proactive monitoring can drastically minimize the occurrence and effects of downtime, ensuring that every customer can make payments when they are willing, able and present.

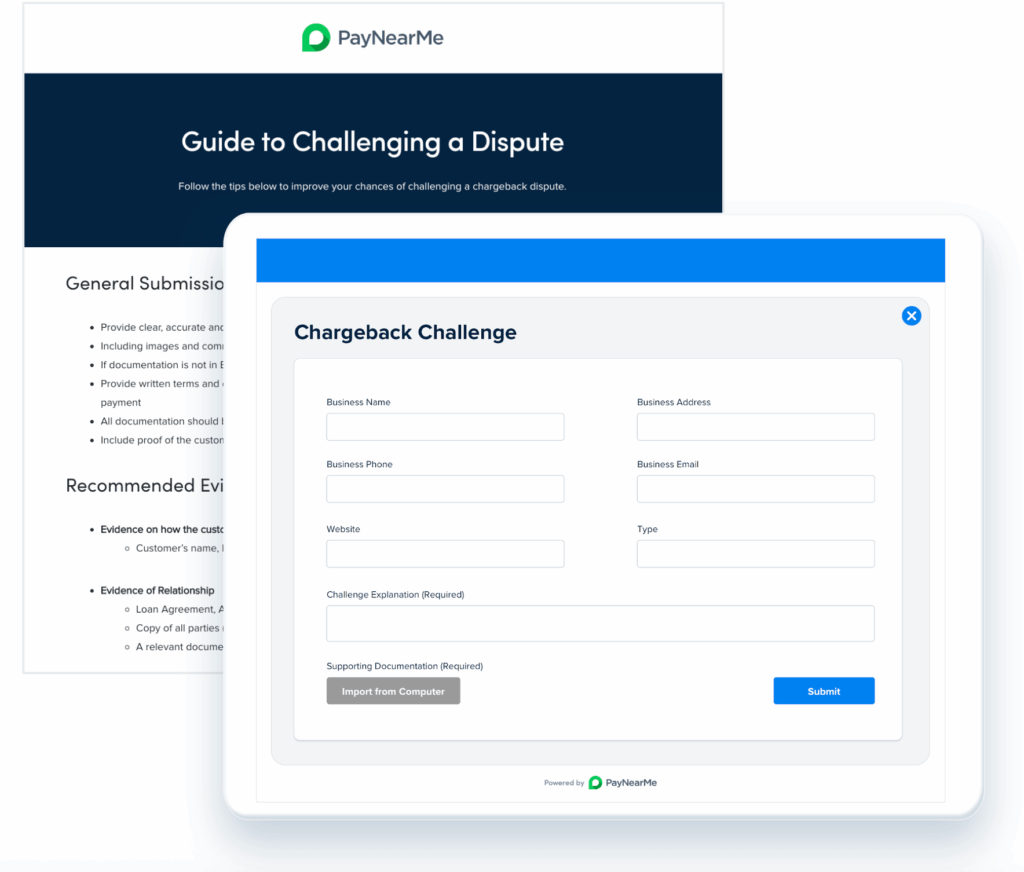

Win more chargebacks with less effort

For chargebacks that can’t be avoided, agencies need to cut down on the resolution process. Modern platforms make it easier to stay organized, gather evidence, submit dispute responses, and track pending disputes.

A growing number of organizations don’t bother fighting disputes due to the lengthy process, leaving money on the table and inviting future chargebacks from repeat offenders. Smarter chargeback tools mitigate that risk.

Fight back against fraud

New artificial intelligence tools can identify and mitigate fraud at scale. Platforms with modern, flexible APIs and built-in fraud engines can provide a significant boost to fraud and risk management in a rapidly changing digital environment.

These tools offer the promise of nuance, helping to push good payers through the payment process while effectively flagging bad actors.

It’s time to reframe the payments conversation in tolling

The tolling industry has long prioritized reliability and continuity—and for good reason. But as volumes grow, payment behaviors evolve and operating costs rise, agencies can no longer afford to evaluate payments solely through the lens of transaction fees.

Understanding the total cost of payment acceptance requires a broader view—one that accounts for transaction costs, people costs and systems costs, and recognizes the outsized impact of payment exceptions in tolling environments.

Payment Experience Management offers a disciplined, practical path forward. By reducing exceptions, improving visibility, and aligning payment operations across channels, it enables agencies to lower long-term costs while improving collections and service quality.

Moving beyond “good enough” payments is not about adopting unnecessary risk. It is about managing payments as a core operational function—and doing so in a way that supports efficiency, compliance and public trust.