Want More On-Time Payments from Millennials? Engage Them on Their Terms.

Competing financial priorities can make it tough for many consumers to make loan payments. Millennials (ages 30 to 44), in particular, face challenges that influence their bill pay behaviors. According to Bank of America, 76% note that high debt interferes with their financial goals, and nearly 60% of this generation are living paycheck to paycheck.

It’s no surprise that 48% of millennials agree that managing and paying bills causes them anxiety, according to PayNearMe’s 2024 consumer report. Our research dug deep to understand how this age group perceives the bill pay experience and key issues that make it more difficult. We also tapped their opinions on capabilities that might help reduce stress and make it easier to pay their loans.

What are some of the biggest loan payment problems for millennials? Here we’ll highlight some key issues, and what you can do to remove friction and cost-efficiently increase acceptance rates. By addressing their unique challenges, you not only build loyalty but also improve profitability through fewer late payments and lower processing costs. To read the full report, click here.

Why millennials struggle with legacy bill pay processes

More than other generations, millennials feel stressed around paying bills. They’re at an age when a range of important life events impact their finances, such as trying to pay off student debt, buying their first home and starting a family.

Millennials are digital natives who thrive on simplicity and speed in every transaction. Unfortunately, legacy bill payment systems often fail to meet their expectations, driving stress and creating barriers to on-time payments. This cohort is accustomed to seamlessly easy mobile ways to pay for shopping, ride shares, splitting the check with friends and more. The bill payment experience, on the other hand, is rarely that simple, and millennials have a very low tolerance for friction.

For example, consider these top pain points:

- Cumbersome payment processes – Millennials are used to intuitive, invisible payment experiences. Legacy biller portals with complicated logins, outdated interfaces and limited payment methods don’t make the cut. These systems increase the likelihood of skipped or late payments, which can lead to costly phone calls and missed deadlines. Each of these phone calls on average costs up to $6 and takes about 8 minutes of your staff’s valuable time, whereas a successful self-service payment may cost only $0.10.

- Remembering logins – For millennials, one of the biggest hassles in paying bills is having to remember logins and passwords for many different websites. 42% of this age group identified logins as a major hurdle making bill pay more difficult. And this pain point is a critical factor driving up the cost of payment acceptance. Our research found that 52% of payment-related calls are about password resets. With modern technology, that friction and the associated costs could be eliminated entirely.

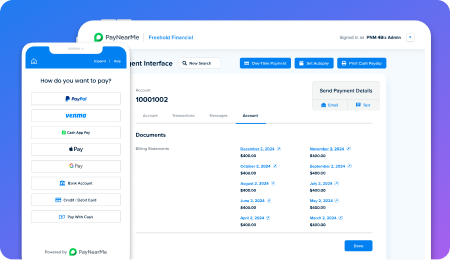

- Lack of digital wallet options – As mobile wallets like PayPal, Apple Pay and Venmo become staples of financial management, millennials expect these options for loan payments too. Yet, many lenders haven’t adopted this flexibility. This generation quickly latched onto mobile wallets to easily make P2P money transfers to friends, vendors, babysitters, etc. Now, this payment method has evolved into a go-to resource for storing cash for future use, including paying loans.

Also worth noting is that millennials like to diversify how they pay, finding it helpful to balance cash flow by paying loans from different sources and using different payment methods. Even more important, 80% of this age group say they will abandon purchases if their preferred payment method isn’t available. That same fickleness may apply to loan payment, making it imperative for lenders to offer a full range of payment options.

What does all this mean for you and your organization? It’s crucial to make your loan the easiest to pay, increasing the probability of getting paid on time and at a lower overall cost.

Modern customers require modern payment experiences

Increasing on-time payments is essential to a lender’s profitability, and making loans easier to pay is an essential way to get there. Major change doesn’t have to disrupt your business; the right payments platform can help solve your biggest challenges.

Let’s take a look at what millennials told us would make it easier to pay their loans on time:

- Timely digital reminders – This age group has a number of monthly bills and find it hard to keep track of them all. Indeed, 43% said they struggle with remembering due dates, indicating a strong need for timely reminders. In fact, 45% of millennials surveyed agreed that receiving reminders via text message or email would help them pay on time.

- Fast, simple, personalized options – Eliminating friction is central to improving acceptance rates. A core improvement is to optimize self-service payments with a personalized, login-free experience. Nearly 80% of millennials surveyed rank it as ‘important’ to receive a personalized link to access their account in the payment app without having to log in. And they expect screens to be pre-populated with their account details so they don’t have to manually re-enter information each time.

Streamlining payments with personalization is a powerful way to improve outcomes, particularly with this age group. Nearly 70% of consumers noted they value a personalized loan payment experience, and 61% of millennials want to receive recommendations tailored to their preferences or situation, such as options to set up autopay or refinance their loans.

- Digital wallet options – A majority of younger consumers are shifting payment habits to mobile wallets, yet bill pay models have been slow to catch up. A modern payments platform, such as PayNearMe, can enable lenders to accept many popular apps including PayPal, Apple Pay, Google Pay, Venmo and Cash App Pay. Providing this flexibility can improve the customer experience, especially with millennials. PayPal has been cited as their preferred wallet, with 70% choosing that app.

Concerned about the cost of wallet transactions? Think of it this way: Allowing customers to pay in ways they prefer—and where they may keep more cash—can help reduce exceptions like ACH declines. It can take many successful transactions to offset the costs related to only one exception (calls, notices, delinquencies, etc.). That’s why it’s vital to avoid issues and non-completed payments that drive up your total cost of acceptance.

Drive down your cost of accepting payments

Getting paid on time, while minimizing the total cost of acceptance and reducing manual intervention, should be a top priority for lenders in today’s market. That’s what an innovative payments platform like PayNearMe is built to help you accomplish.

We help you quickly deliver the frictionless, flexible self-service payment experience that helps millennials (and all your customers) pay on time, with fewer exceptions. With automated workflows and data-rich reporting, you can maximize back-office efficiency to further drive down your total cost of accepting payments.

Explore the PayNearMe platform with our interactive virtual demo or schedule a personalized demo.