Slice of Finance Recap: Lowering the Total Cost of Acceptance with Payment Experience Management

Originally published by Slice of Finance.

Danny Shader, Founder & CEO at PayNearMe, recently joined Jared Taylor on the Slice of Finance podcast to discuss how PayNearMe reduces the true cost of acceptance by focusing on Payment Experience Management.

You can watch the full video version below, or read a version of the transcript below that has been shortened and edited for readability using AI and human editors.

Jared: Danny, so great to have you on the podcast! How are you doing today?

Danny: Really good; it’s good to be here.

Jared: I’m excited to have you. It’s your first time ever being on the show, so what I usually like to do with first-time guests is if you could tell the audience a little bit about yourself and your company, and then we will go into our conversation today.

Danny: Sure, I’m Danny Shader. I’m the founder and CEO of PayNearMe, and we are the creators of payment experience management, which I’m sure we’ll talk about at length.

Jared: So, a question I usually ask many guests is you’re walking down the street—let’s say you had a PayNearMe t-shirt on or some sweatshirt with the logo—and you gave me the tagline, but let’s say you always run into some people that keep asking me “Oh, that’s interesting,” and keep asking you question after question. Give me that kind of full breakdown for the very interested person that wants to learn more about PayNearMe.

Danny: I like the way you put that. We do what we call Payment Experience Management, and that’s managing everything about how our clients—who are typically billers—collect and disperse payments from their consumers.

And we’re doing that with the objective of one thing, which is driving down the total cost of payment acceptance. So, most people tend to think about the cost of payments as like the cost of processing, and it turns out that’s not what matters at all. That’s basis points. The real money is in what happens if a person doesn’t pay. That’s incredibly expensive to a biller, also for the costs of interacting with three constituencies: obviously, that consumer making a payment, the customer service agent who’s maybe supporting them or contacting them if they didn’t make a payment, and people on the back office who are reconciling and settling payments when something doesn’t go right. That’s where all the money is.

And if you can make sure that everything goes right, and if something goes wrong, make sure it’s managed as easily as possible, you can dramatically improve the economics of payment acceptance to reduce the total cost of payment acceptance. And, it’s not something that people light up about when I’m at a cocktail party, but if you’re the person responsible for the income statement of your company, you care a lot about this if you’re a biller.

Jared: Let’s talk about worst-case scenario of someone not using PayNearMe. What does that worst-case scenario look like?

Danny: Well, I’m just going to guess that you’ve got a bill on your desk right now. Maybe it’s from a medical company or something else; it’s probably some $30 copay or something, and I bet they didn’t make it very easy for you to pay. And I’ll bet, as a practical matter, you never pay that bill. So, that’s bad. The other one that’s bad is you do go to pay, and then maybe you don’t have sufficient funds in your account, and now you’re bouncing, and that’s costing a lot of money to the person you’re billing. I mean, there’s just an incredible amount of money in the go-wrong case, and it’s something nobody ever thinks about.

Let’s just talk about Payment Experience Management. Consumers absolutely expect a phenomenal payment experience when they’re doing a commerce transaction. You expect the experience when you check out of Amazon to be really seamless. When you take Uber, you expect it to be seamless.

I’m willing to bet that when you go to pay your bill or your toll or repay your auto loan, you’re not expecting that experience to be great. We’ve sort of, as a populace, have this idea that if we’re doing commerce, it should be great; if we’re not doing commerce, it should suck.

And frankly, if you can make the “not-suck” thing great, that’s got a huge economic upside, because there’s literally trillions of dollars spent in billing. And if you think about this for a second, in commerce, if you don’t make the payment, they’re not going to ship you the good.

But in billing, they’ve already delivered the good; they’ve already incurred the expense, and now they just want to get repaid. And if they don’t let you repay it, that’s a loss. You want to make sure that goes smoothly.

Jared: Let’s talk a little bit about some of these billers that continue to not make it easy. The logic behind that—it’s like you already provided a service; you want people to pay you. Why wouldn’t that experience be perfect or as easy as possible for you to get paid?

Danny: Well, if you think about it, for a biller to be paid, like you’re an auto lender or something, you’re terrified of anything breaking that system. You’ve got this thing that’s working as crappy as it is, and it takes courage to want to improve it.

So that’s not going to be the first thing you’re thinking about. And probably inside your organization, the person who’s responsible for marketing or brand who recognizes, by the way, that that billing experience is probably the primary interaction that that biller is having with their client, that person is separated from somebody over here in treasury who’s responsible for the system, and that person’s afraid of anything going wrong.

However, when somebody else in that category, some competitor there delivers a great experience, and then an executive sees that and goes, “Well, why aren’t we doing that?” then everything changes.

By the way, we have a great client, Santander Consumer, which is a big auto lender. Don Smith, who’s the CTO there, has a line which I love. He says, “I have a word for CIOs who don’t innovate—I call them unemployed.” And I think that’s increasingly true. When execs see that there’s a better way and the company’s not doing it, there’s a lot of pressure to do it.

Then, of course, if they know that this other vendor, this other competitor was using PayNearMe and they know it’s successful, then we become trusted. They’re willing to take that risk of getting involved in the system. And then, as Don would also say, you need to have executive sponsorship all the way through that transition process. But once you do it, the benefits are massive.

If you think about those savings on a monthly basis to the biller, that’s an annuity of savings that never ends, assuming we keep doing a good job for them—which we will.

Jared: Danny, before we started recording, you and I were chatting a little bit about when these billers have a poor process to collect the money they’re owed. Sometimes it can even feel like it’s such a bad process it almost feels like a scam. And they’re not trying to scam you; they’re just trying to get paid because they do it so poorly. That’s probably a newer problem because we are getting a bunch of people worrying about phishing. I’d love to hear your thoughts on this.

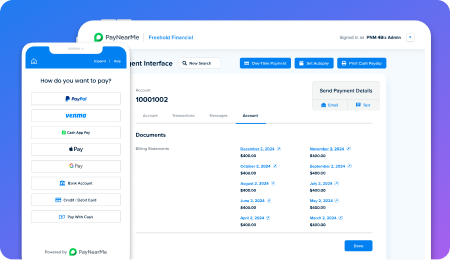

Danny: If somebody gives you a phishing attempt, they want to extract account credentials from you, right? They want to extract payment information. We sent you a PayNearMe Smart Link QR code. If you take a moment to scan that—I don’t know if you can do that now—but if you can, tell me what you notice when you scan that.

Jared: It goes directly to a site. It doesn’t go to some other random link for something I’m not expecting to pay for. It tells me my account details, my payment due date, my amount due, my amount past due, any late charges, the total amount. I can set up my default.

Danny: What didn’t you have to do?

Jared: I didn’t have to give them any information.

Danny: Right, so you know that’s not a scam. They know about you; you’re not giving them the information. And the reason that’s the case is because our system has already—in the background—extracted all the information we need to know about you before we send you that QR code.

As opposed to these links you get on a bill where there’s a QR code and you scan it and it says, “Now give me all your information.”

First of all, that’s incredibly inconvenient, and people aren’t going to pay—that’s not easy. And secondly, it creates this opportunity for phishing. What you just saw there ensures somebody’s going to pay and you know you’re not being phished.

Jared: Some of the phishing attempts, too, are like “You owe us this, did you pay yet?”

Danny: Yeah, exactly. Because that’s so simple, the other thing you’re not going to do is you’re not going to pick up the phone and call them. The number of times people are calling for login help or authentication purposes—think about what that costs. A customer service call costs more than $10 an instance, sometimes $20. That’s super expensive.

Jared: Continuing on that, why is end-to-end payments—like that journey—now in focus for many billers?

Danny: Honestly, it’s just the economics of the income statement. The entity wants to be as profitable as they can be. Typically, they’re thinking about the cost of goods sold, but what they’re not thinking about is the cost of customer service.

A huge amount of customer service expense for a biller is in the payment experience. So, the reason why we created this notion of Payment Experience Management is we recognize it’s a black hole for dollars. If we can make that experience better, we can reduce the total cost of payment acceptance and ensure that people get paid. That’s a huge win for our clients and obviously really good for our business.

To go back to that link you scanned—the reason it’s incredibly hard to make a process that simple, for you to have seen what you just saw there, we had to be implemented in the background. We were extracting information out of the system of record, normalizing it, processing it, and presenting it in a way that you could pay with any form of tender. You could pay with your cards, your ACH, Apple Pay, Google Pay, Venmo, Cash App, even cash with our proprietary walk-up network, where you just scan a barcode at a register. Making all of that happen for thousands of billers, none of whom have the same backend, is incredibly hard, and it’s what we’ve spent the last 17 years creating.

Jared: How can businesses lower the total cost of acceptance by eliminating something like exceptions?

Danny: Let’s start with the obvious one—the person doesn’t pay because you make it hard. Like the bill that’s sitting on your desk you don’t touch for a service that’s already been provided; that’s clearly expensive.

Secondly, if you are motivated to pay and you have money but your money is sitting in Venmo this month and the vendor doesn’t accept Venmo; you’re not paying the bill. You’ve got to present people with every form of tender, and you’ve got to do it in a way that’s super simple, so they don’t have to know their login credentials, which they probably aren’t thinking about when paying a bill. That’s just at the consumer level.

Now, when the customer service agent interacts with you, how do you make it simple for them when you’re on the phone and they send you a text link in real-time to complete the payment?

Then, all this stuff is coming back in; the money is coming in, files are being presented, and you want to make the back office as efficient as possible. How do you make reconciliation, settlement, and chargebacks as simple as possible? There’s a shooting gallery of opportunities to improve processes if you understand what goes wrong and then use technology to solve it.

Most people want to self-serve if you can make it incredibly simple.

Jared: Danny, talk about how the payment experience is that final moment of brand reputation.

Danny: Sure. Think of something like your auto loan. You probably never interacted with the auto lender directly; you interacted with the dealer who sold you the vehicle. Your only interaction with the lender was your billing experience. Many people set up loans on auto payment, but they’re actually in the minority.

Most Americans are making that billing payment every month, which means their interaction with that lender—their sense of the brand—is that recurring billing experience. God forbid they have a terrible customer service experience on top of it.

If you make that easy and delightful, like the classic Uber example, that accrues to the benefit of the brand that cared enough to deliver a great payment experience.

Jared: You had me scan a QR code during the demonstration—why a QR code?

Danny: By the way, that QR code is just a token. We could have given you a magstripe, a link on your phone, or sent you an email.

Jared: What do you see as the most common?

Danny: When people are interacting with customer service agents, we see text being common. They’re on the phone with the agent expressing a willingness to pay, and they get the link and make the payment. Then maybe we automatically set you up on autopay if you’re the right client for that.

If you’re doing print and mail, you want to be in a QR code. You want to have the right modality in the right circumstance. You’ve got all these people interacting with the biller in different ways with different payment methods. You want to give them the easiest way to pay with the right form of tender when they have the funds.

Jared: Last question—what’s next for PayNearMe?

Danny: More and more of the same. Payments are fractal—the more you understand them, the more you realize there’s more to do. Any place where there’s an expense or a missed payment, we want to solve that. You’ll see us leveraging AI to improve these processes for our billers.

Jared: Danny, thanks so much for joining me today.

Danny: I really appreciate it; it’s really fun.