Why Banks are Slow to Evolve and Why Data-Driven Opportunities Make Change Imperative

Many banks and lenders believe their payments model is not ‘broken’ because they aren’t receiving regular customer complaints, so there’s no need to fix it—or evolve it, for that matter. However, their capabilities may be far more limited than they think, and lost opportunities could be stacking up. If financial institutions (FIs) are not capitalizing on their data for decisioning insights, they may not understand what improvements are critical to acquiring and retaining more customers, and improving business performance.

Particularly in the highly competitive lending market, FIs need to keep pace with evolving consumer expectations. That means focusing on data at the customer level: understanding behaviors, attitudes and preferences that influence choices and payment activity. And perhaps more importantly, using those insights to deliver the personalized experiences that customers want.

So why aren’t more financial institutions optimizing their data strategies and capabilities? And how can they overcome barriers to change, and keep pace with new technologies and market trends?

Recently PayNearMe partnered with Datos Insights to explore those questions in surveys and interviews with consumer lending executives from banks, credit unions and consumer lending companies. The executives surveyed cited that improving efficiencies and customer experience (CX) remain top priorities. However, none of them are prioritizing data maturity as a path to get there. That could be a crucial mistake. According to a recent IDC report:

“Companies that have adopted mature data practices achieve 2.5x better business outcomes across the board. Significant increases were seen for revenues and profits, efficiency, higher NPS scores and lifetime customer value.”

Driving digital transformation in an organization can be tough and get stalled by a variety of challenges, yet the payoffs can be significant, so let’s unpack it. Along the way, we’ll touch on what financial institutions can do to speed progress toward improving CX and unlocking value from their data.

Barriers to Innovating Payments and Data-Driven Decisioning

Legacy Infrastructure and Technical Debt

Many FIs have spent decades stacking up technology investments and are now hamstrung by an ecosystem that is siloed, complex and expensive to change. And the larger the organization, the slower the pace of change. McKinsey noted that large banks are 40% less productive (in product rollout cycles) than digital-native fintechs and neobanks. They added that, being less agile and carrying more ‘technical debt’ may cause banks to “give up on their digital transformations rather than attempt to overcome the barriers.”

An added dimension is that payment and data technologies are evolving rapidly, and the pace may be too fast for traditional financial institutions. It’s a compelling reason why many banks and credit unions are now partnering with fintechs that offer specialized solutions that help them remain competitive as capabilities and compliance needs change.

Cultural Resistance

Another reason financial institutions are slow to adopt new technologies is the industry culture. Particularly with payments, if the business is getting by with traditional functionality and processes, it can be hard to get people on board for change.

In the study, most of the lending executives said their current payment capabilities were adequate. They did recognize that customers now want faster, more convenient options like they use elsewhere, such as Venmo, PayPal, Apple Pay, Google Pay and CashApp. Yet almost none of those lenders offer these new payment methods.

Organizations may get stuck focusing on the challenges of implementing new payment rails and new processes. However, the business case gets considerably more compelling if FIs factor in the significant value they can gain via insights by tapping into hundreds of data points in every transaction. The right fintech partner may be able to solve both problems.

Lack of Data Access and Expertise

That leads us to another major obstacle: many FIs cannot even access usable data. Of those we surveyed, 77% agreed that managing multiple payment platforms makes it very complicated to collect data.

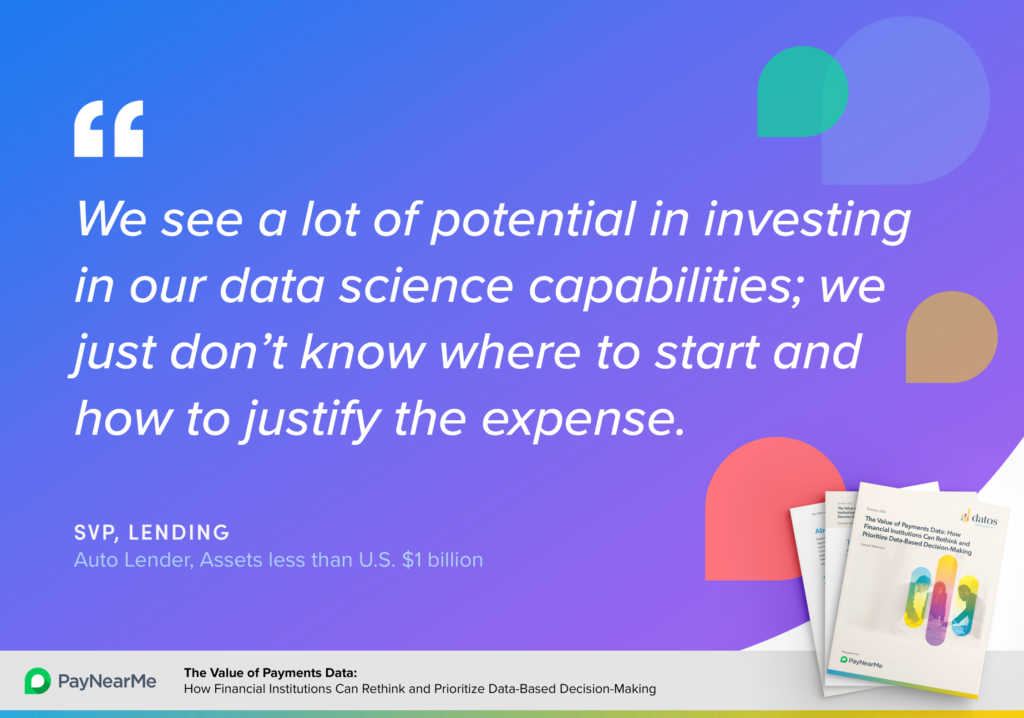

Adding to the challenge, even if FIs could access their data, most lack the in-house infrastructure and expertise to make the most of it. A recurring theme in our research was that banks and lenders have identified the opportunity, but have insufficient resources to transform data into actionable insights.

A Deloitte study echoed this finding, noting that two of the top three challenges organizations face are limited data skills (71%) and poor data literacy (54%).

Unable to Make the Business Case

Another monumental challenge impeding adoption of new technologies is building buy-in with leadership. Particularly in lending organizations where regulatory compliance and risk management are top priorities, it can be tougher to make the business case for change.

Now add the fact that the value derived from solutions for capturing and analyzing data may be harder to quantify than revenue-generating products. According to Deloitte, one of the top challenges Chief Data Officers face is building buy-in with executive committees to invest in better data management and advanced analytic capabilities.

Speeding Up the Path to Opportunity

The old adage, “You don’t know what you don’t know” applies to many organizations that are not putting their data to work. For example, 67% of executives we surveyed felt that managing multiple payment platforms did not impact the quality of their customer experience, but they also confirmed they were not leveraging data from those transactions. What insights are they missing that could be used to make CX more personalized and better meet customer needs, or help reduce delinquency and default?

The power of AI and machine learning (ML) can enable dramatic leaps forward, and a scarcity of data science capabilities doesn’t mean FIs need to stick with the status quo. Partnering with outside experts, like PayNearMe, can help organizations extend their payment offerings and tap into a wealth of diverse data to uncover insights for making better decisions that drive bottom-line improvements.