Personalization Strategies to Boost Auto Loan Repayment

Repos are up. Delinquencies are rising. And in the middle of it all, Buy Here Pay Here (BHPH) dealers are bearing more risk than ever. With vehicle repossessions hitting 1.73 million—levels not seen since the 2008 financial crisis—delinquent auto loans aren’t just a customer problem— they’re a profitability problem.

There’s never been a more important time for Buy Here Pay Here (BHPH) dealerships to make the payment process as frictionless as possible—and that takes a Payment Experience Management approach that meets today’s demands.

TIP: For a deeper dive on this theme, view our recent webinar on-demand here.

The hidden cost of poor payment experiences

The problem isn’t just delinquency—it’s the experience borrowers have when trying to pay.

Legacy payment systems make even simple tasks feel like a hassle. Confusing interfaces, forgotten passwords, and limited payment options create friction that drives up your cost of acceptance.Take one example: every failed ACH payment might cost you just cents in transaction fees, but the real price—NSF fees, support time and manual cleanup—can push the cost past $20. And when frustrated customers call to make a payment by phone? That’s $8 per call, compared to just $0.10 for self-service, according to Gartner.

Phone payments cost up to 80x more than self-service channels

Gartner

Unfortunately for your bottom line, these aren’t edge cases. Nearly 1 in 5 consumers regularly call to pay their loan—and it’s not just older generations. A surprising number of younger borrowers (ages 18–29) are picking up the phone, too. That’s a sign something isn’t working.

What’s needed is a new approach. Payment Experience Management optimizes every payment touchpoint—across customers, agents and operations—to reduce exceptions, automate processes and dramatically lower your total cost of acceptance.

Up next, we’ll break down how modernizing and personalizing your payments strategy can transform your bottom line—starting with how (and where) your customers want to pay.

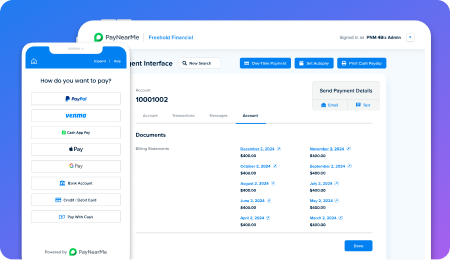

Fill critical payment gaps with alternative payment options

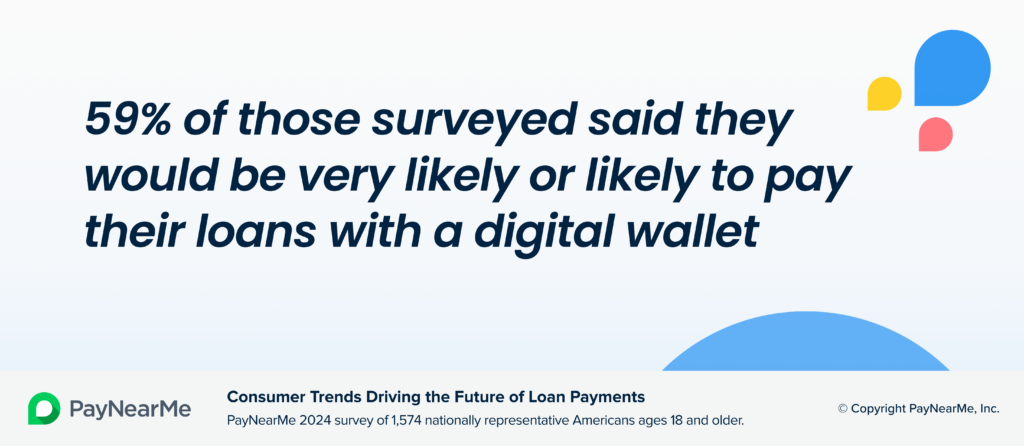

As a lender, you may think exceptions and delinquencies are always rooted in your customers’ limited cash flow, but these issues also come from rigid payment processes that cause friction. The one-size-fits-all approach of getting everyone to use ACH is obsolete. Consumers increasingly prefer to pay with digital wallets such as PayPal, Venmo and Cash App Pay.

Our survey found that nearly 59% of consumers would be very likely or likely to pay their loans with a digital wallet. And it’s not just younger generations. 64% of consumers aged 45-60 also want to pay bills with wallets. A critical factor is that many people now keep a cash balance in a mobile wallet for future use. 38% of consumers said they would use a stored balance to pay their loan, if that was an option. This number jumps to 47% with lower income individuals who may be unbanked and use their digital wallet in lieu of a bank account.

When people are struggling to get by and may deprioritize their auto loan, it’s essential for your dealership to offer wallet options that can make it easier to pay. Offering the payment types your customers want provides a frictionless experience that reduces agent support calls and failed payments—ultimately lowering your total cost of acceptance.

Have concerns around usage, security, and implementation? Check out our recent webinar where we debunk five common myths about mobile wallets.

It’s been surprising how many people actually use PayPal, Venmo, Google Pay, and Apple Pay. We’re seeing a constant upward trend in the forms of payment our customers are using.

Operations Manager, Heritage Acceptance Corporation

While we’re talking about alternative options, let’s not forget cash. Particularly for lower income and unbanked borrowers, paying loans with cash is still important. However, it can be challenging for customers to get to your dealership during business hours, especially if it’s far from their home or work. And as a BHPH dealer, you know that accepting cash or money orders in person is costly, increases risk and consumes staff time that could otherwise be focused on more complex needs.

With a modern payments platform, you can enable customers to pay loans in cash at convenient retail locations where they already shop, such as 7-Eleven, Walmart and CVS. It makes life easier for them and increases the likelihood that you will get paid on time.

Hyper-personalize the experience to drive positive outcomes

Offering more payment types is essential to help reduce exceptions and delinquencies, and meet more of your customers where they are. However, choice is not enough. Consumers are now accustomed to hyper-personalized experiences, and they expect that same personalization when paying their loans. In fact, nearly 70% of people we surveyed said it’s important to have a personalized experience where the platform recognizes them and tailors the billing information.

Not yet focusing on hyper-personalization at your dealership? Small steps can have a big impact. The more you simplify the payment experience with personalized options—the more likely customers will pay on time, on their own. That means less exceptions, less intervention, less cost.

Here are some key examples:

- Send a digital reminder (via text message or email) about payment due dates to solve a major pain point and improve outcomes. 41% of consumers say keeping track of due dates is challenging and 47% agreed that getting a reminder would make it easier to pay on time.

- Provide personalized, no-login access for making payments. Why? Here are several compelling reasons. Consumers find it difficult to remember logins, and that frustration often translates into calls that increase your costs. PayNearMe research found that 52% of payment-related calls were for password resets. It underscores how an outdated system creates more hassle for customers and derails agent productivity to deal with mundane tasks instead of high-value work.

- Pre-populate payment screens. People resent having to retype account details every time they pay their loan. The vast majority expect payment screens to be personalized, with 80% of consumers noting it’s important to have their payment details (loan number, amount due, etc.) pre-populated.

The right modern payments platform can help you provide this type of personalized, frictionless experience. Digital reminders can be automated and your agents can push them directly to your customer via text or email. Each message can include a unique, personalized Smart Link™ that gives that customer one-click access into their account with no login required. From there, they can choose their preferred payment method and be done in seconds. Tools such as Smart Link aren’t just convenient—they dramatically reduce call volume, failed logins and missed payments.

Hyper-personalization can significantly improve on-time payments and lower your overall cost of acceptance. For example, when Drive Now Acceptance implemented the PayNearMe platform, they pushed hard to convert customers to use Smart Links. Now 77% of their customers use them for self-service loan payments, helping the dealer dramatically cut costs.

Make autopay work for real life

Migrating your customers to recurring autopay is ideal, if everyone uses it and 100% of payments process as planned. But neither of those things happen, especially with legacy payment systems, because options are so limited.

Many consumers need more flexibility or they won’t commit. In fact, 65% of people we surveyed avoid setting up autopay because they want more control over when their bills get paid. And equally, 65% said that having more flexible options would make them more likely to enroll in autopay.

Choice and personalization (two strategies we highlighted above) are essential to drive autopay adoption. With a modern platform, your customers can choose how and when automatic payments will occur, to better fit their cash flow schedule. For many borrowers—particularly subprime—a fixed autopay date doesn’t work.

Offering split payments and pay-date flexibility isn’t just “nice to have”—it’s a key way to reduce late payments and lower collections costs. Customers can also vary the payment method, which is helpful if they keep money in multiple places (e.g., bank account, digital wallet, cash in hand).

Interested in more stats on autopay adoption? See our infographic.

Don’t forget your back-office

Poor payment systems don’t just hurt customers—they can cripple your operations team.

Manual reconciliation. Exception handling. High call volume. These tasks devour hours and resources every day. However, with a modern platform, reconciliation can shrink from a full workday to minutes.

This is where the operational side of Payment Experience Management excels: by automating workflows, minimizing manual effort and giving your staff time back to focus on what matters most—relationships and driving revenue.

Improve BHPH profitability with a better payment experience

Your BHPH dealership may be all about delivering exceptional service, but driving profitability is key. To sustain that, you need to get paid on time, at the lowest cost, with the least exceptions and manual intervention. That’s what a modern payments platform like PayNearMe is purpose-built to do.

Seamless access and flexible options enable you to provide a frictionless payment experience, and automated workflows help maximize efficiency for your back-office.

See the PayNearMe platform in action. Explore on your own with our interactive virtual demo, or contact us to request a personalized demo.